Regain Financial Freedom

Debt can feel overwhelming, but with the right strategy, you can systematically eliminate it and regain financial freedom. This guide explains the two most popular methods: Snowball and Avalanche.

Debt can feel overwhelming, but with the right strategy, you can systematically eliminate it and regain financial freedom. Two popular debt payoff methods - the snowball and avalanche strategies - offer different approaches to tackling multiple debts. This guide will help you understand both methods and choose the best approach for your situation.

Understanding Debt Payoff Strategies

Both the snowball and avalanche methods involve making minimum payments on all debts while putting extra money toward one specific debt at a time. The difference lies in which debt you prioritize.

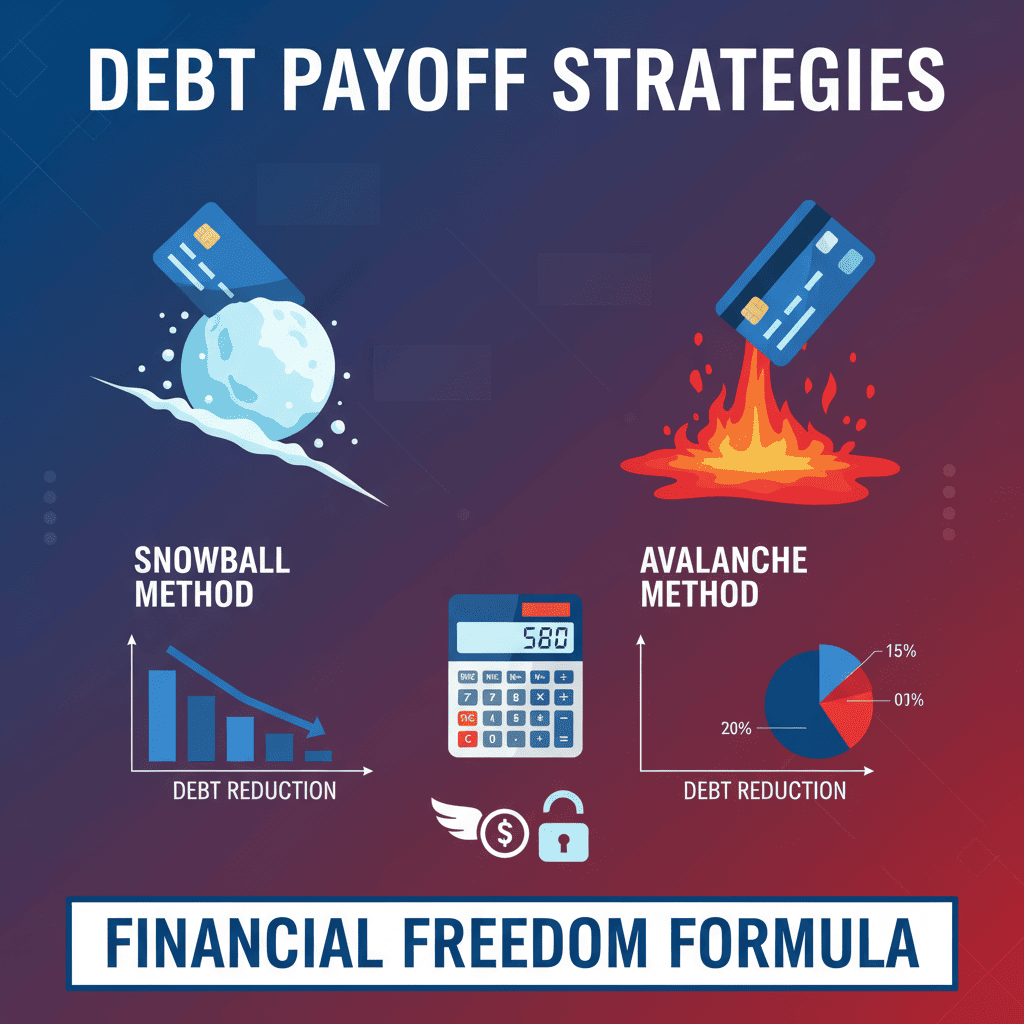

Debt Snowball Method

Focus on paying off your smallest debt first, regardless of interest rate. Once eliminated, move to the next smallest debt.

Pros:

- Quick psychological wins

- Builds momentum

- Easier to stay motivated

- Simplifies debt portfolio

Cons:

- May cost more in interest

- Doesn\'t prioritize high rates

- Mathematically suboptimal

Debt Avalanche Method

Prioritize debts with the highest interest rates first, potentially saving more money in the long run.

Pros:

- Saves more in interest

- Mathematically optimal

- Faster debt elimination

- Lower total cost

Cons:

- Slower initial progress

- Requires more discipline

- Can be discouraging

Pro Tip: Compare Your Options

Use our debt payoff calculator to compare snowball vs avalanche methods for your specific situation and see which saves you more.

The Debt Snowball Method Explained

The snowball method focuses on paying off your smallest debt first, regardless of interest rate. Once the smallest debt is eliminated, you roll the payment amount into the next smallest debt, creating a "snowball" effect.

How It Works:

- List all debts from smallest to largest balance.

- Make minimum payments on all debts.

- Put any extra money toward the smallest debt.

- Once the smallest debt is paid off, add that payment to the next smallest debt.

- Repeat until all debts are eliminated.

Psychology Matters: The snowball method leverages behavioral psychology. Quick wins create momentum and motivation, making it easier to stick with your debt payoff plan long-term.

The Debt Avalanche Method Explained

The avalanche method prioritizes debts with the highest interest rates first, potentially saving you more money in the long run.

How It Works:

- List all debts from highest to lowest interest rate.

- Make minimum payments on all debts.

- Put any extra money toward the highest interest rate debt.

- Once the highest rate debt is paid off, move to the next highest.

- Continue until all debts are eliminated.

Mathematical Advantage

The avalanche method is mathematically superior because it minimizes the total interest paid over time. For disciplined individuals focused on saving money, this approach offers the best financial outcome.

Which Method Should You Choose?

The best method depends on your personality, financial situation, and motivation style:

Choose Snowball If:

- You need motivation and quick wins.

- You\'ve struggled with debt payoff before.

- You have several small debts.

- Psychological factors are important.

Choose Avalanche If:

- You\'re motivated by saving money.

- You have high-interest debt.

- You\'re disciplined and patient.

- Mathematical optimization appeals to you.

Additional Debt Payoff Tips

- Create a Budget: Track income and expenses to find extra money for debt payments.

- Stop Using Credit: Avoid adding new debt while paying off existing debt.

- Consider Consolidation: Simplify payments and potentially reduce interest rates.

- Increase Income: Side hustles or overtime can accelerate your timeline.

- Build an Emergency Fund: A small fund prevents new debt from unexpected expenses.

- Get Support: Share your goals for accountability and encouragement.

Real-World Example: Snowball vs. Avalanche

| Debt | Balance | Interest Rate | Min. Payment |

|---|---|---|---|

| Credit Card A | $2,000 | 18% | $50 |

| Credit Card B | $5,000 | 22% | $125 |

| Personal Loan | $8,000 | 12% | $200 |

| Total | $15,000 | - | $375 |

Snowball Order: Credit Card A → Credit Card B → Personal Loan

Avalanche Order: Credit Card B → Credit Card A → Personal Loan

The Result

With an extra $500 monthly payment, the avalanche method saves approximately $800 in interest and eliminates debt 3 months faster than the snowball method.

Conclusion: Your Path to Financial Freedom

Both the snowball and avalanche methods can effectively eliminate debt. The snowball method provides psychological benefits and momentum, while the avalanche method saves more money mathematically. Choose the method that aligns with your personality and stick with it consistently.

Remember, the best debt payoff strategy is the one you\'ll actually follow through to completion. Whether you choose the emotional satisfaction of the snowball method or the mathematical efficiency of the avalanche method, the most important step is to start today and remain committed to your debt-free journey.

Success Tips

Celebrate small victories, track your progress visually, and remember that becoming debt-free is a marathon, not a sprint. Stay focused on your long-term financial freedom goals.